Fintech Multiples Redux

Originally published on my Substack December 23, 2021

In Q3 of last year the market for early growth-stage-backed fintechs started to look a little manic. I took a look at some of the data for publicly traded comps to get a sense of just how much growth was being baked into these financings and wrote about it. Some of you enjoyed that piece so I thought I’d get to work on a sequel.

Note: The calculations are described in my previous post. Numbers may have shifted slightly since then due to rounding and earnings adjustments but are directionally the same. The level of precision is more than adequate for this rough and ready approach.

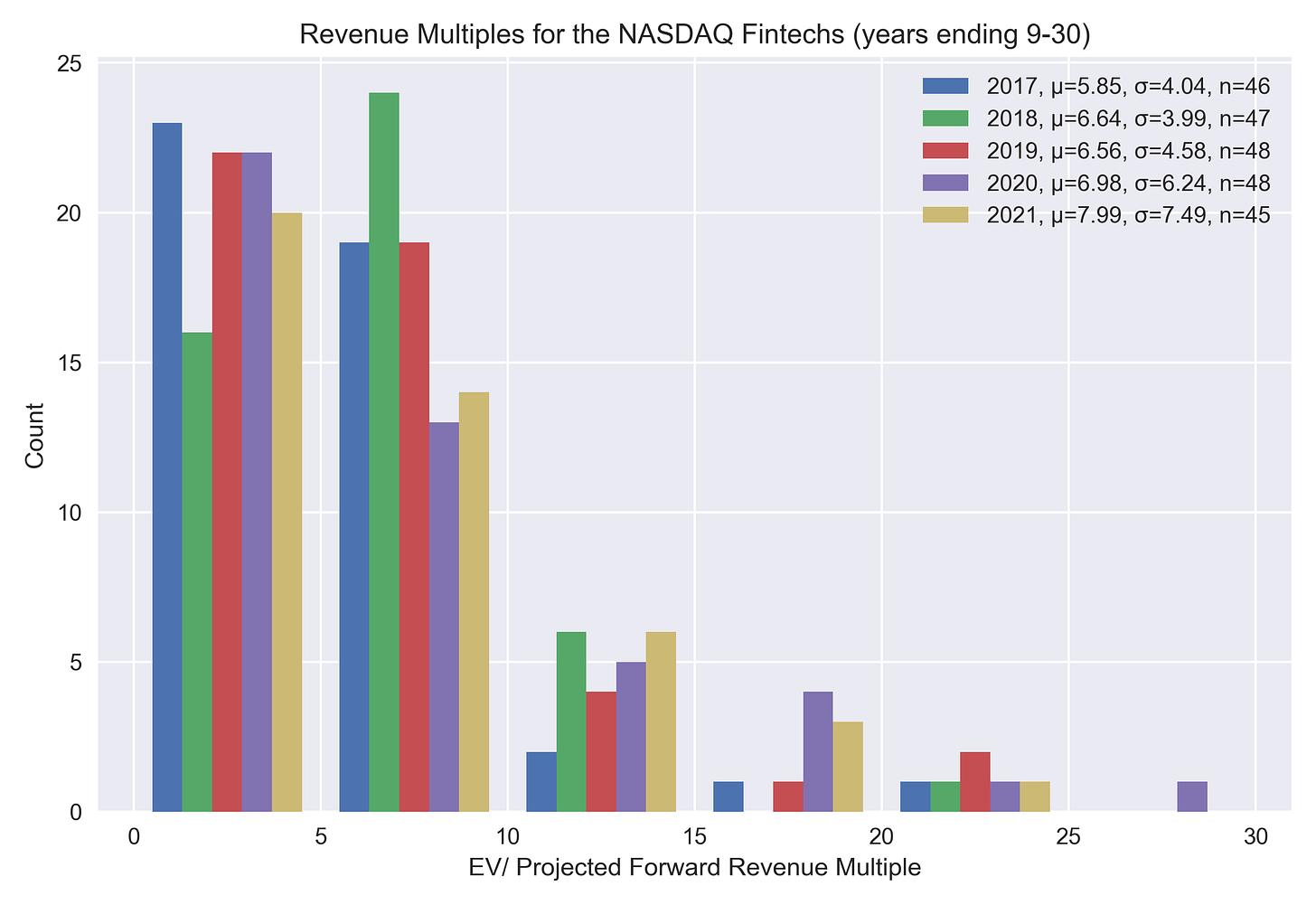

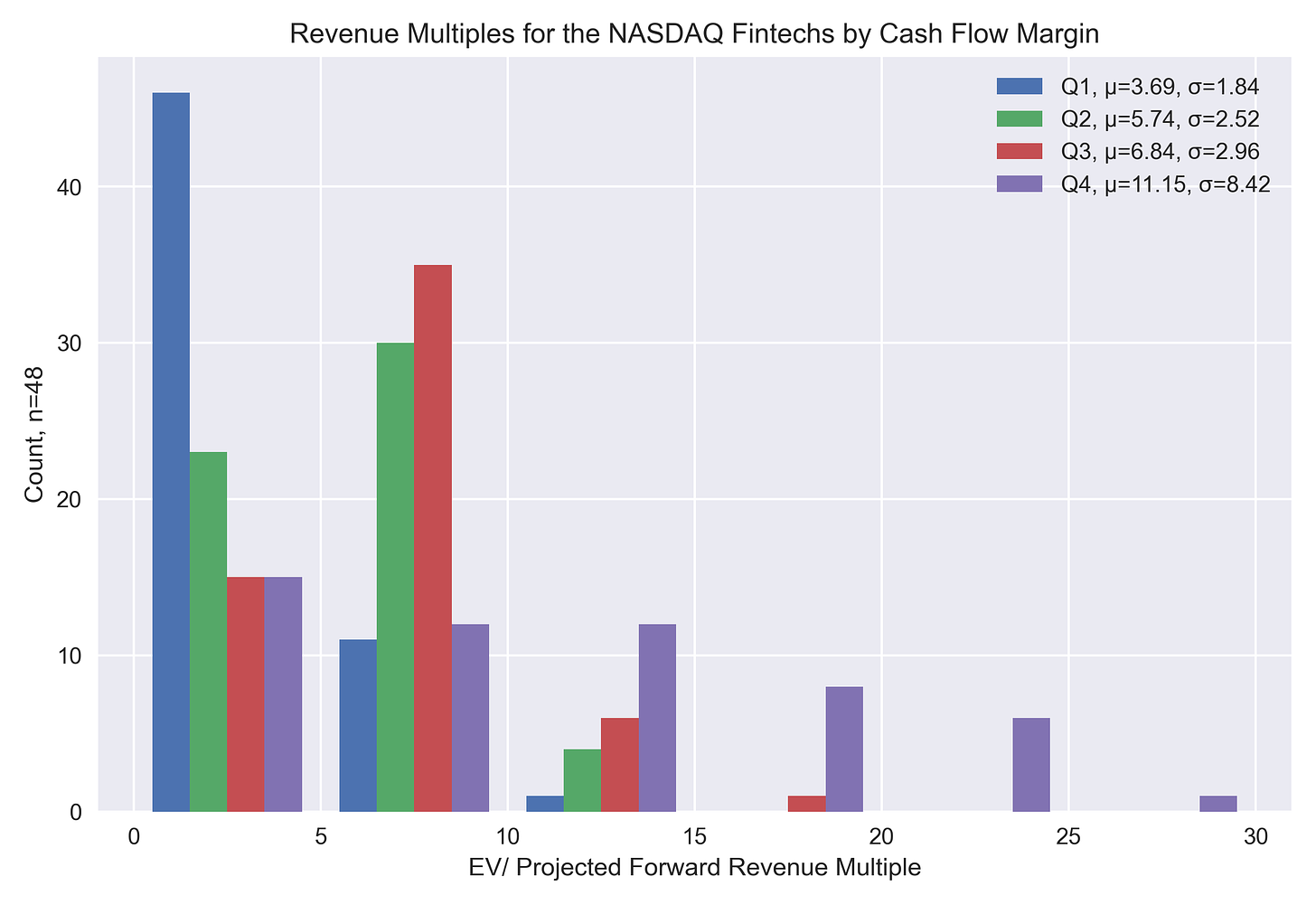

The histogram above shows the number of companies in the NASDAQ Fintech index who’s forward multiples fall into the buckets on the x-axis. The legend includes the average forward multiple and standard deviation for each year denoted by the Greeks mu and sigma respectively. The lowercase n in the legend refers to the number of stocks that we have data on for that time interval.

As we observed last year, there is a persistence of late-cycle characteristics with higher forward multiples and greater dispersion within the category (valuation multiples are heteroskedastic like most financial variables). While gaining modestly, the average fintech still trades at roughly half the multiple of a public SaaS company (at least until a couple of weeks ago).

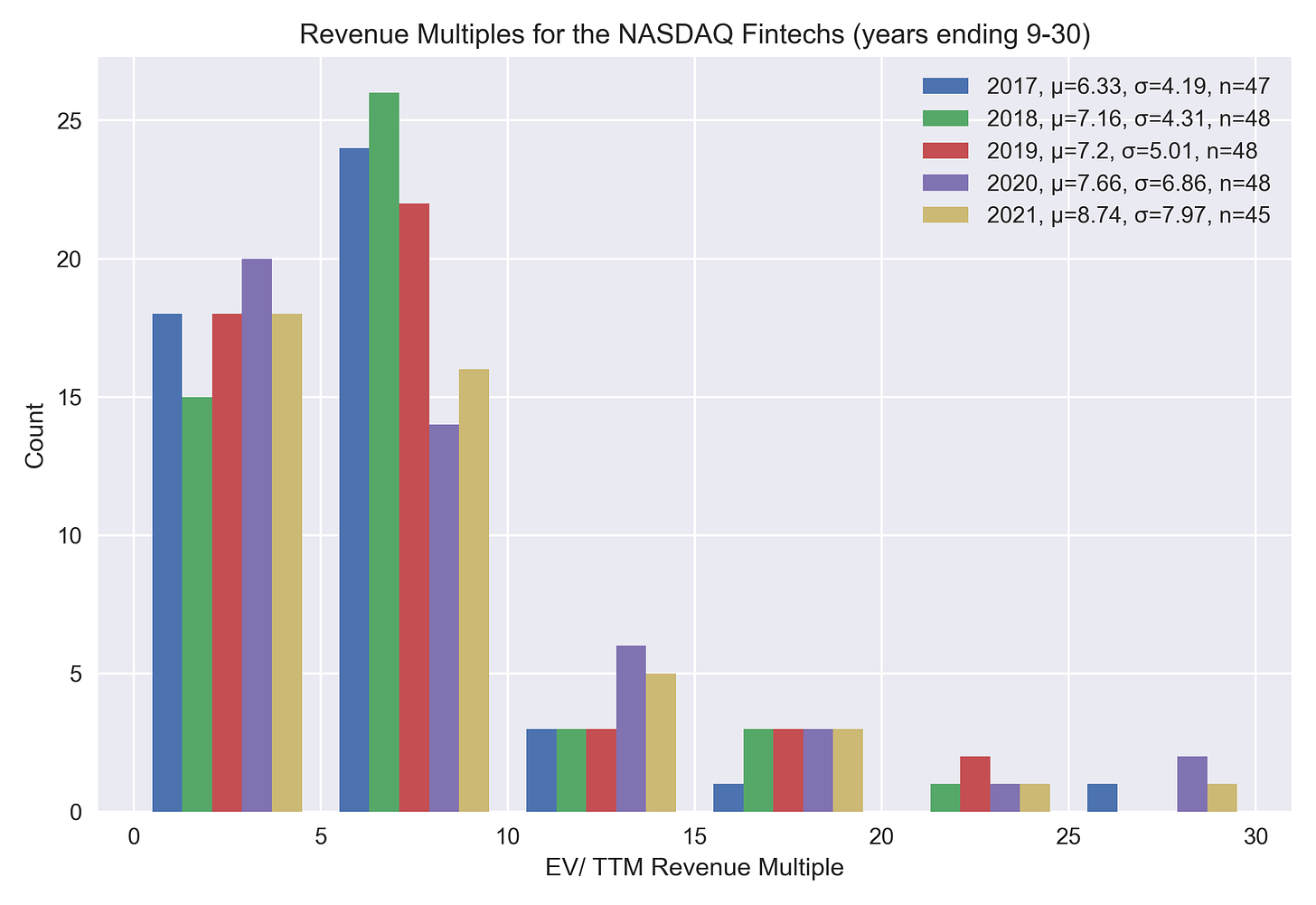

Above we see the same trend as a function of TTM revenue (the ratio of enterprise value to revenue is higher as TTM leaves out next year’s forecast revenue growth).

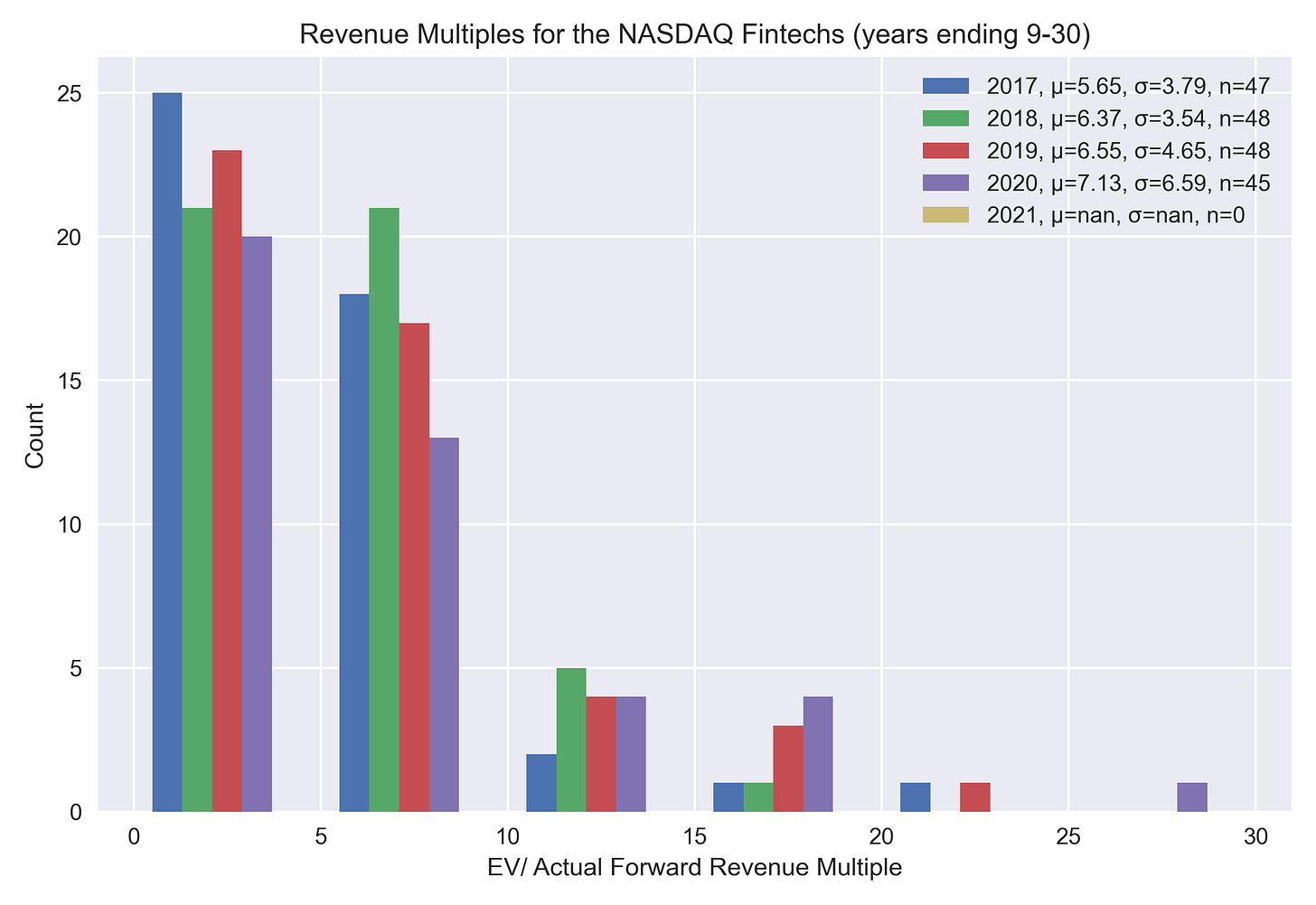

Looking at valuations over actual NTM revenue (where in Q3 of 2020 the average fintech was trading at 7.13x the observed revenue over the subsequent year), valuations continue to stretch and fail to keep pace with expectations (if modestly).

Presumably no one is astounded by the information that a high-margin, asset-light business category is expensive on a historical basis; now consider the jamboree the private markets have been holding. Last quarter, the median valuation multiple for venture-backed fintechs was 19.5x up from 16.0x in Q2 of 2020 (it’s worth keeping in mind that the average would be materially higher as the distribution of valuation multiples is right-tailed).

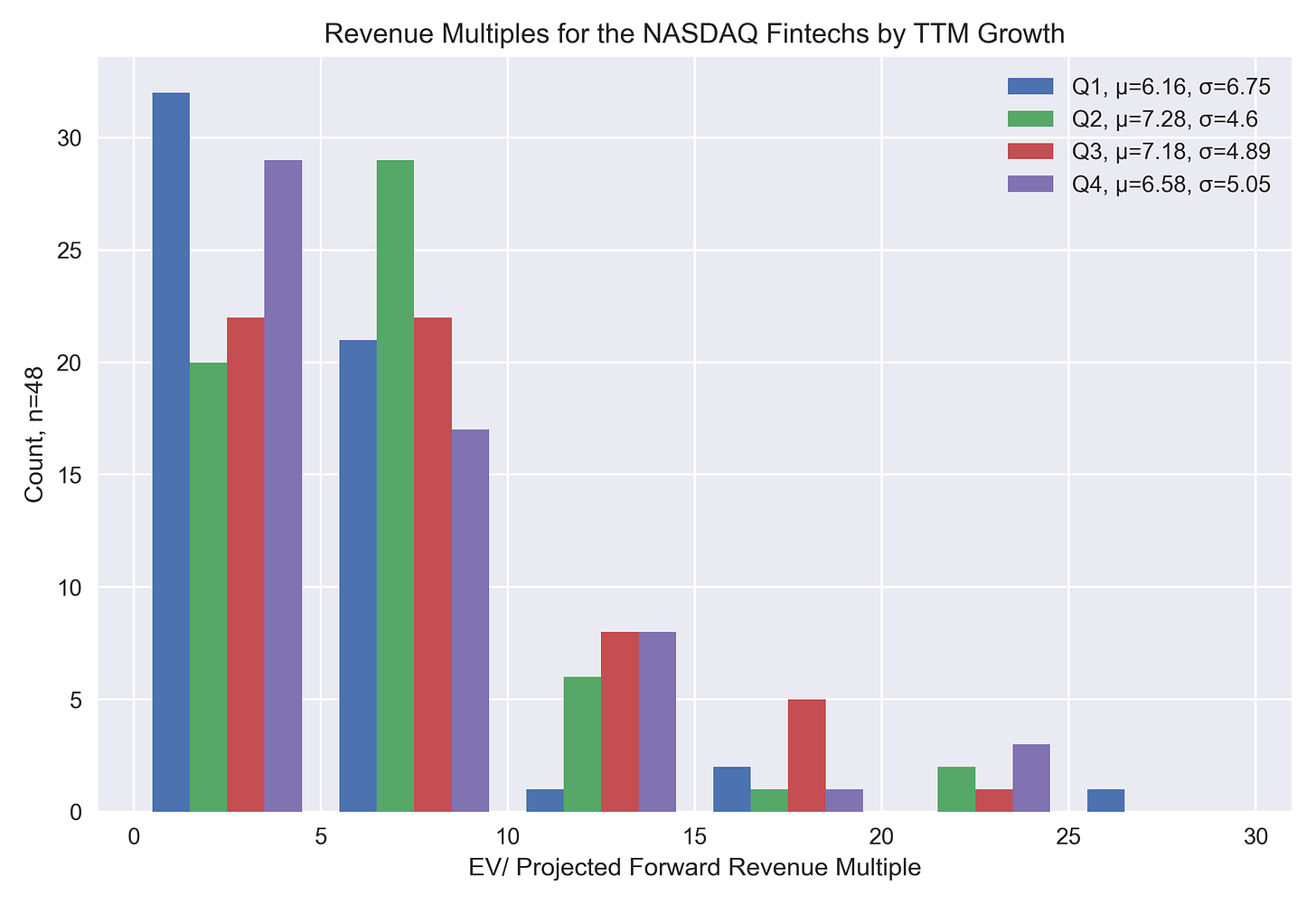

There are a few ways to cut this data which can arguably produce a more appropriate comparison to a privately-held peer set; one is by bucketing the tickers by growth. When I did this exercise last year I was surprised to find that the top quartile fintechs by TTM growth had a lower forward multiple than the second quartile. This year is even odder with the third quartile fintechs being the most valuable on average.

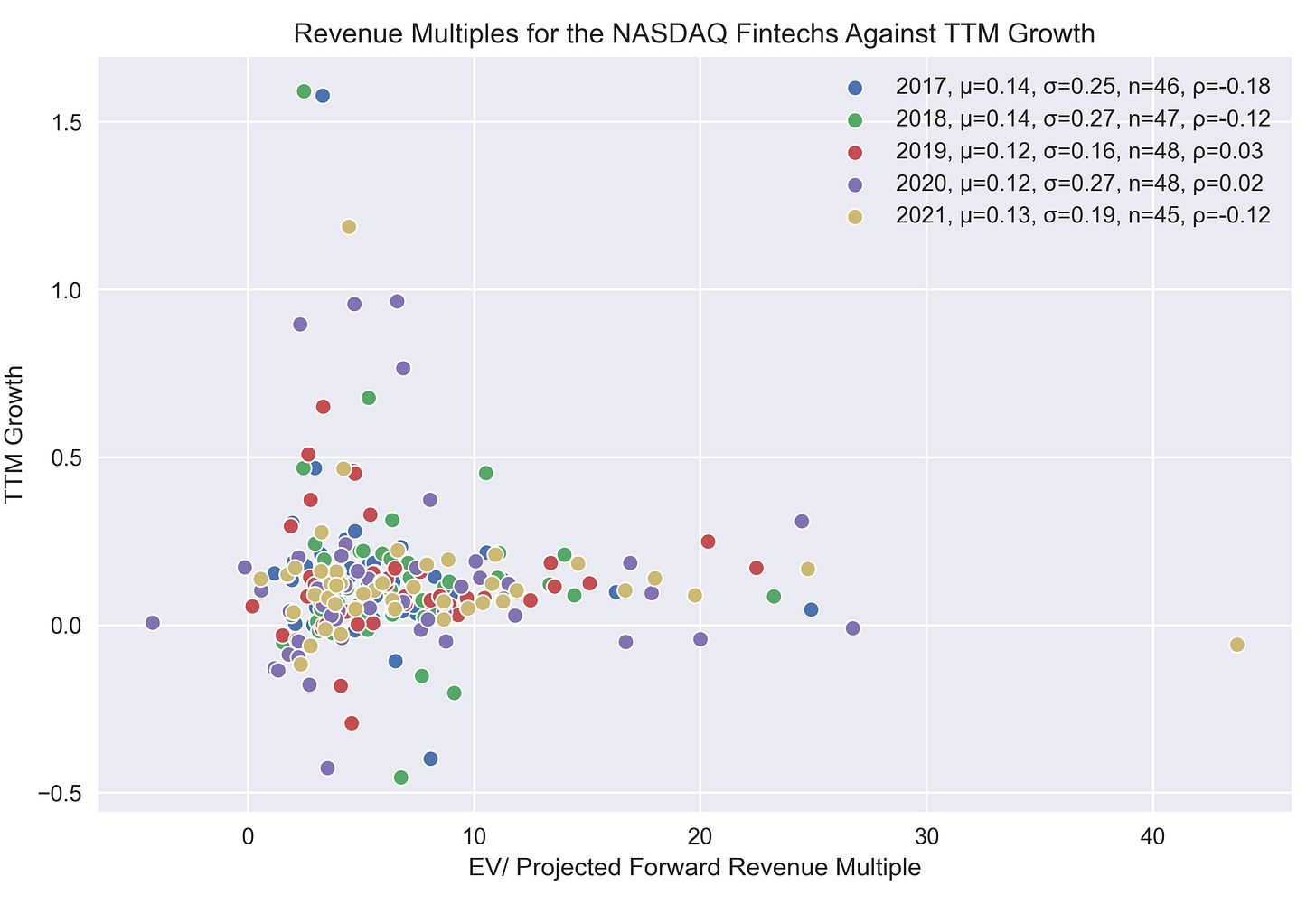

Investigating this relationship another way, I plotted TTM growth against forward multiples: no relationship (Greek mu = average; Greek sigma = standard deviation; Latin n = sample size; Greek rho = correlation coefficient).

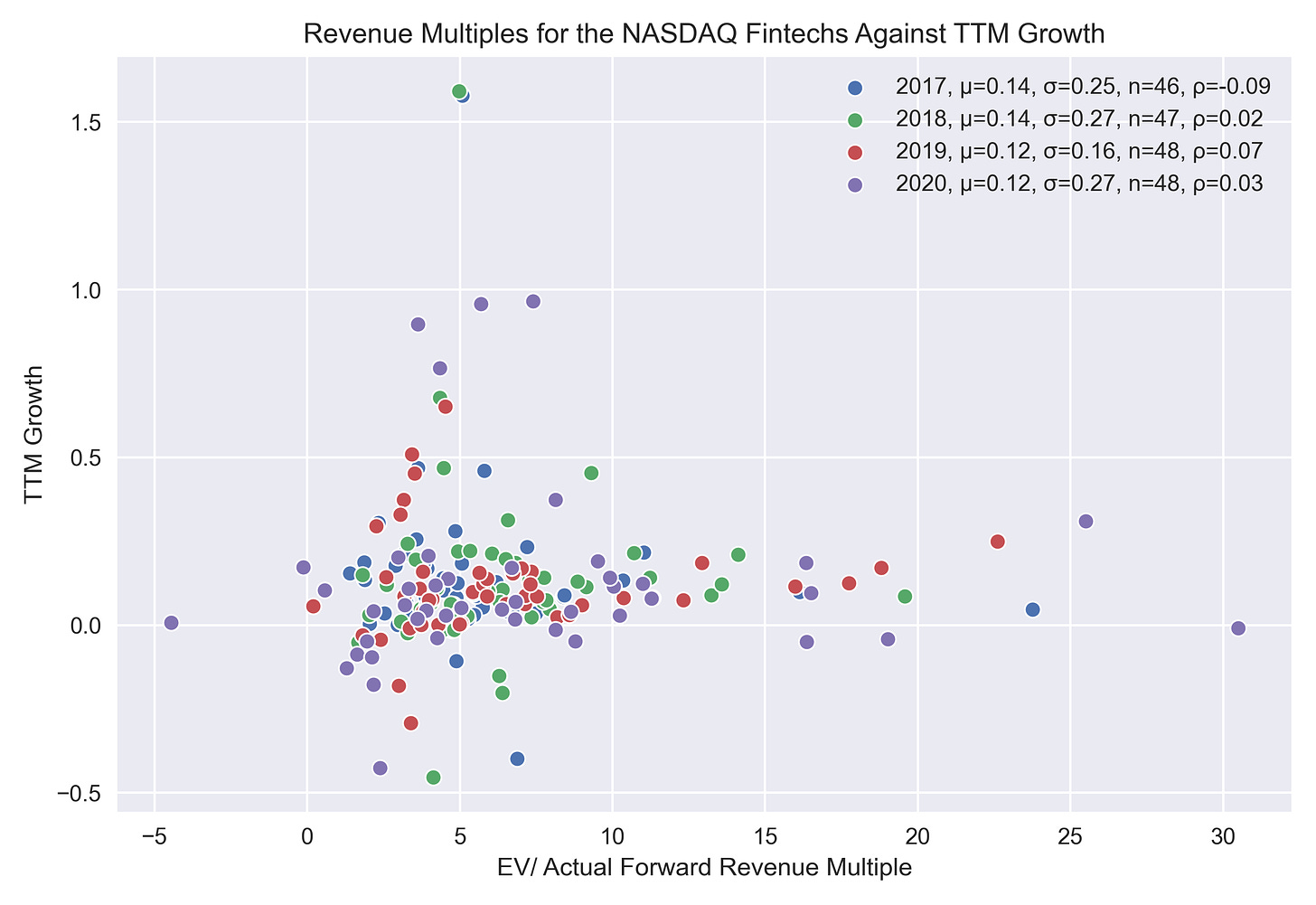

And when double checking my estimate against realized revenue produces the same result.

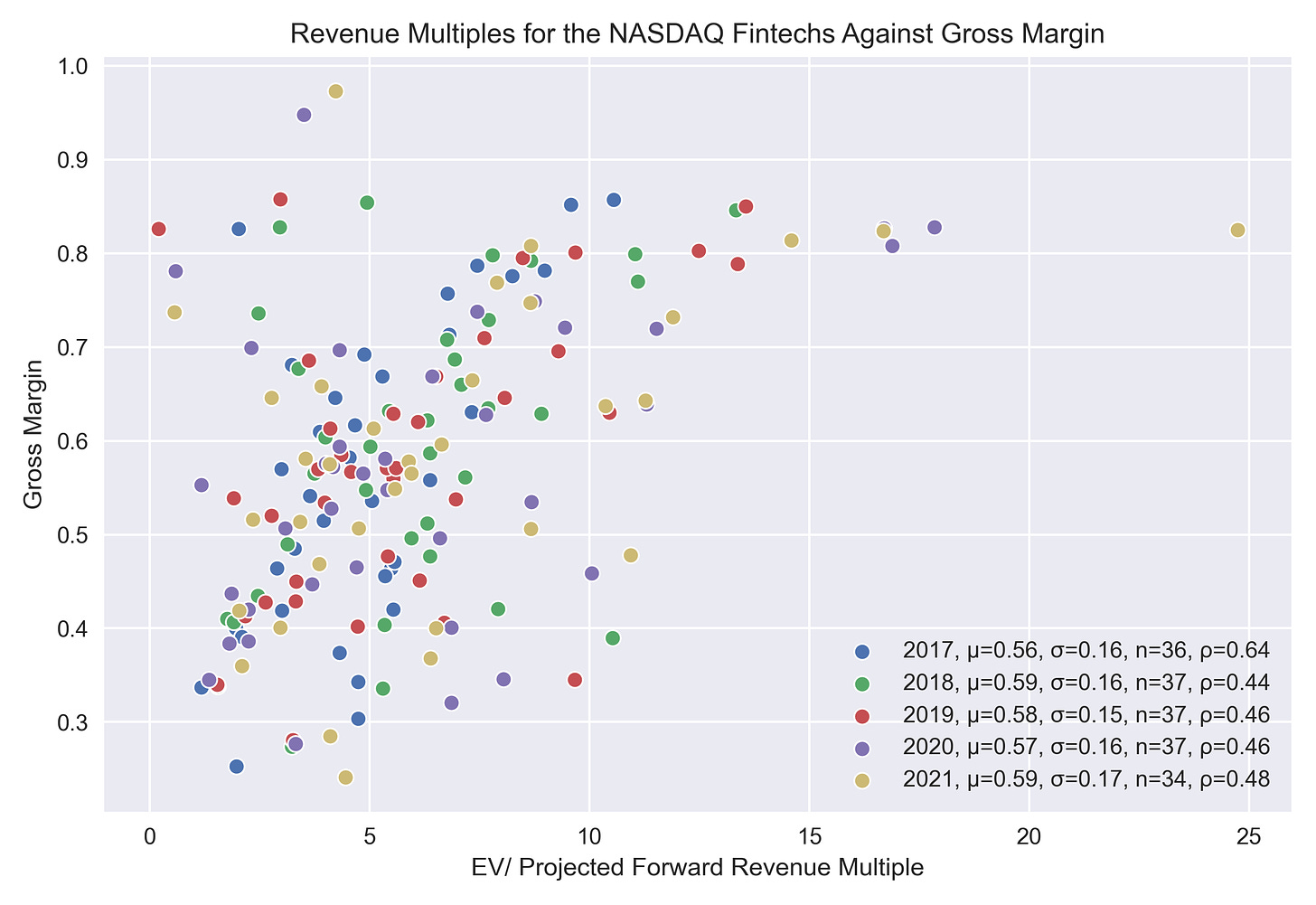

Gross margin is one of the more important metrics VCs (especially early-stage) look at when evaluating fintechs as they provide a convenient mapping to the type of fintech business you’re looking at. Fintech is a more complex category than SaaS as the businesses range from tech-enabled digital insurance companies with sub-30% gross margins to software subscription businesses for FIs with 90% gross margins. A company’s gross margins tell you how much of what the company sells is technology and how much is a financial product. These are crucial inputs to the valuation.

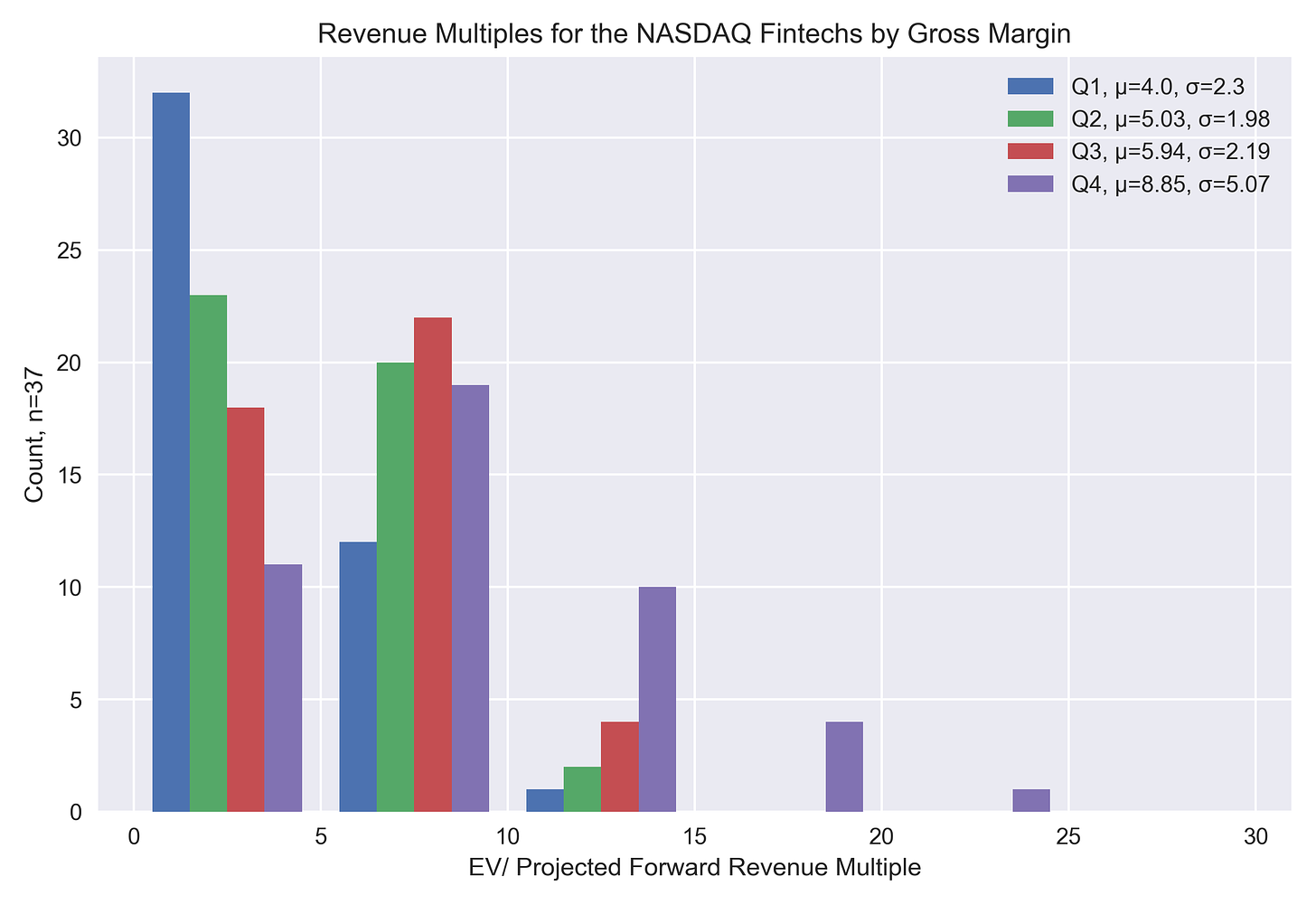

The public data confirms this though as not all publics report COGS we lose a lot of our data points. The other important takeaway here is that fintechs are sub-60% gross margin businesses on average compared to roughly 75% for pure SaaS.

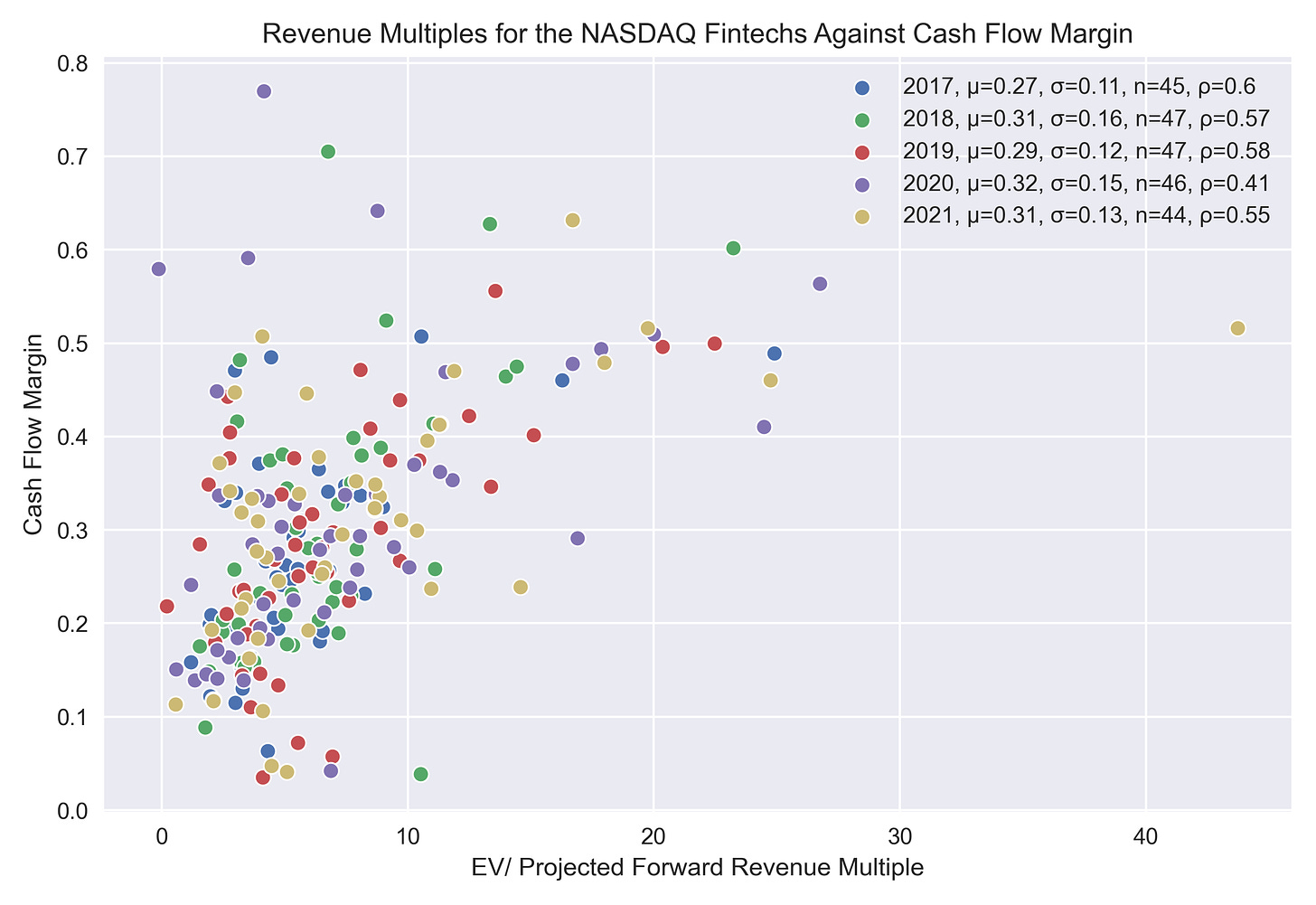

In the past I’ve written about cash flow margin as a proxy for the “SaaSy-ness” of a mature fintech company and the relationship is even stronger now than a year ago. The “SaaSy-est” fintech companies are trading at 11x forward multiples just like SaaS businesses. Notice last year’s correlation of 41% increasing to 55% over the past year in the chart below.

Note: This metric has minimal bearing for early-stage investors as we’re happy to have our portfolio companies burn cash to massively accelerate growth.

If we assume that the expansion stage financings are happening for “SaaSy” fintechs (which is not unreasonable), it’s even safer to assume that the average valuation is more than 2x their public equivalent.

I started this research by asking a vague question: roughly how much growth is baked into these frothy fintech venture rounds? I’m pleased to end with a simple if rough estimate: at least 100%.

Addendum: Wag the Dog Look-Back

This doesn’t warrant a separate post and if you’ve made it this far I’m assuming this will also be of interest. As it’s the end of the year it feels cathartic to provide a brief retrospective on one of my other markets-focused essays.

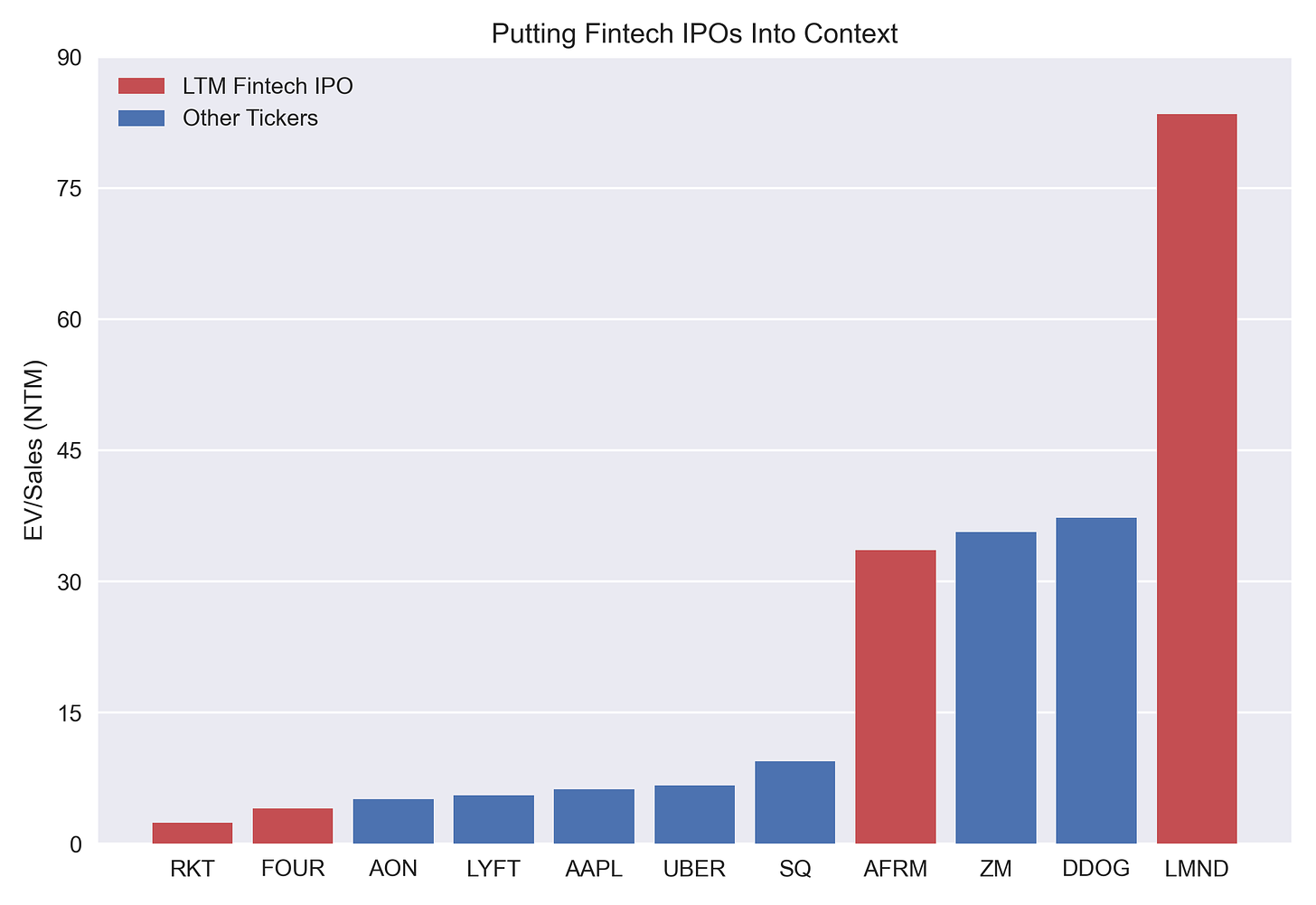

In Q1, I wrote about the baffling performance of the recent fintech IPOs. I’ve included a chart from that piece below which shows the revenue multiples for the tickers on the x-axis the week of February 15th, 2021.

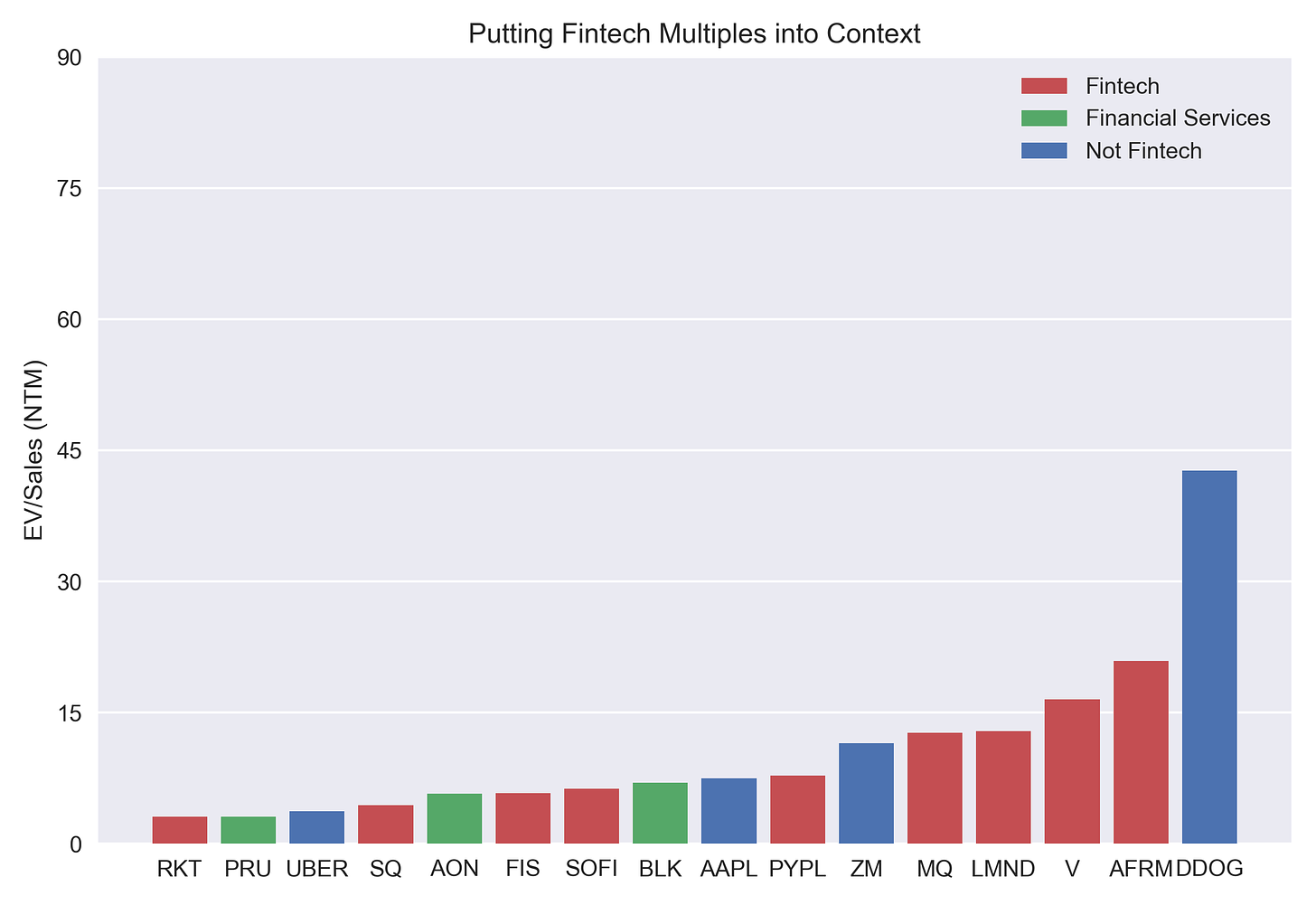

And below this I’ve added a chart with the same tickers (with a few relevant additions) and the same y-axis scale using today's prices.

At the time I was astounded that anyone was paying over 75x forward revenue for Lemonade (12.7x today) and similarly puzzled by Affirm’s 30x multiple (20.0x today). It turns out I wasn’t the only one.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.